Note: Following the publication of an article on Community Reinvestment Areas in December, I received several follow-up emails asking for clarification on the mechanics of the program. I hope this article provides a more complete summary of the situation. More background on the Bluff Dwellings CRA can be found here.

It’s been over a year since consultant Cody Deeter began advising San Juan County on Community Reinvestment Areas (CRAs), and the program has stirred up a good bit of controversy. At the most basic level, CRAs provide an economic development incentive, and according to Deeter, they can be thought of as “a catalyst for growth.” CRAs are common in Utah. There are 125 active CRAs in Salt Lake County alone, and they’re often seen as an important tool for giving local governments some control over where and how development occurs.

There are no active CRAs in San Juan County but two proposals currently under consideration. A reinvestment area in Blanding has been created by the Blanding City Council, and another area in Bluff was designated by the San Juan County Commission. The Blanding proposal includes a potential Marriott that’s being backed by Phil Lyman and his partners, and it appears to be a fairly standard use of a CRA program. According to the Salt Lake County website, CRAs are “typically used to remove urban property blight, add new jobs, or develop vacant land.” The Blanding City Council, acting in their capacity as a Community Reinvestment Agency, has singled out a zone north of town, which some have called “blighted,” for CRA designation. The area includes multiple property owners and businesses, including an existing restaurant and the vacant site of the proposed “flagship hotel.”

There are different models for CRAs, but most commonly developers pay the full cost of horizontal infrastructure improvements upfront (utilities, streets, curb and gutter, etc.). In return, 75 percent of the taxes the developer pays on the increased value of the land are deferred for 20 years or until the agreed upon infrastructure costs are reimbursed. If the developer does not increase the land’s tax value, they still have to foot the bill for the improvements.

In the case of the Blanding CRA, for example, the developers would pay $1.25 million to install a suite of infrastructure upgrades. If the business is successful, the tax value for the land would shoot up. The school district currently receives $1,759 in annual tax revenue from the property in the Blanding CRA. That number could increase, according to the reinvestment agency estimates, to $50,000 annually after the area is developed. Blanding City and the county commission have already agreed to move both CRAs forward, and they are now waiting on an interlocal agreement from taxing entities, including the school, health, and water districts. Since the school district receives the majority of property tax revenue in the county (roughly 70 percent), its support is critical to advancing the deal. The school board has not yet voted on either CRA.

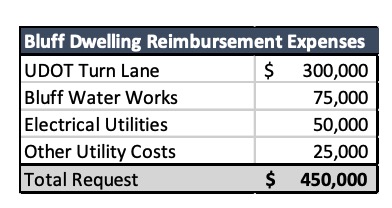

For the Bluff Dwellings CRA, a powerpoint presentation given to the school board lists the costs laid out in the chart below.

Which businesses qualify for CRA benefits?

Deeter told the school board in July, “The common expression used is the ‘but for’ test. ‘But for’ you [the school district] providing increment this project wouldn’t happen.”

“I think that has to be met in order for you to say, yes, we’re going to participate,” he continued. “There has to be upside beyond what could be considered just a handout…You can’t just give people money because they asked for it.”

Deeter went on to argue that the Blanding CRA meets the ‘but for’ test, which Lyman echoed when he recently told the San Juan Record that his project would likely fizzle without a CRA. The idea is that without a tax incentive, lenders will be less likely to back the potentially risky Marriott in Blanding. (Of course, there is much to consider beyond the initial “but for” test. The school board has raised several compelling questions about the Blanding proposal, including whether the development could hurt other businesses in town and lead to minimal net gains in overall tax revenue for the school district. These appear to remain open questions.)

In an ideal situation, a business which needs a CRA incentive to build would be able to start the project with the help of taxing entities. The development would increase the tax value of a given parcel of land, and the entities would gain more revenue in the long term than they would have without the CRA. In turn, the local government can direct development to blighted areas.

The Bluff Dwellings situation is a less common application of a reinvestment program. The CRA boundaries were drawn around a single business, which was not necessarily a blighted section of town, but a lightly developed staging area for a raft company and, in developer Jared Berrett’s words, “sagebrush.” Construction began on the project in 2017, long before the CRA program was even established in the county, which complicates the “but for” test.

So, would the project happen without a CRA? Berrett told the school board in July that without a CRA he will go bankrupt, but construction has continued to move forward even without the CRA’s approval. In order to unpack the history of the project, I compiled a timeline from school board, county commission, and planning commission meetings minutes.

Another note: My hope is that this the breakdown provides some clarity for community members on the context of the project. If this were simply related to the actions of a private business in Bluff, this level of scrutiny would be unwarranted. But the school board’s decision has the potential to determine the fate of up to $450,000 in tax revenue that would flow to the school district if the business opens without a CRA. Berrett told the county commission his Bluff Dwellings Resort and Spa will create 20 jobs if it opens at full capacity, which breaks down to $22,500 in tax incentive per job created.(The dates used as citations for Berrett’s quotes refer to presentations he gave to the county commission on 5/15/18 and to the school board on 7/10/18.)

A Timeline of the Bluff Dwellings Development

Prior to 2013 – UDOT stops paying for turn lanes on large developments, and shifts the burden to the developer. In 2013, for example, the Canyon Country Discovery Center built utilities infrastructure and turn lanes a year before work began on the main buildings in 2014.

c. 2014 – Berrett begins to plan the Bluff Dwellings Resort and Spa, a 54-room complex with pool, smoothie shack, interpretive panels, hiking trails, and options for outdoor tours (more info here).

2015 and 2016 – After approaching 15 lending institutions over 18 months, Berrett finds lenders for the $6 million project. His initial budget, he later told the commissioners, was no longer accurate by the time funding was secured since bids (e.g. for concrete) have gone up. (5/15)

December 2016 – As he’s applying for a building permit with the county planning commission, Berrett receives word from UDOT that he needs to pay for the construction of a highway turn lane. Berrett approaches the planning commission and (according to the commission minutes) receives approval for “phase one” of Bluff Dwellings, the construction of 18 units based on UDOT’s agreement for the maximum number of units that can be built without a turn lane. CRAs or other tax incentives are not mentioned in the minutes.

Early 2017 – Berrett returns to the planning commission and asks for approval for the full 54-unit resort, which will require the construction of turn lanes. The commission grants the full permit. CRAs or other tax incentives are not mentioned in the minutes.

2017 – With permit in hand, Berrett begins construction in Bluff.

December 2017 – Cody Deeter attends San Juan County commission meeting to, according to minutes, “explain what a CRA is and gave several examples of CRAs within the State of Utah.”

February 2018 – Natalie Randall, the county Economic Development Director, and Deeter discuss making the Bluff Dwellings project the county’s first CRA at a county commission meeting.

May 2018 – The county commission hosts a public hearing on the Bluff Dwellings CRA. Berrett presents for several minutes. Six Bluff residents and business owners, and one Blanding resident, make comments. Most ask the county commission not to adopt the CRA plan; some remain neutral. Commissioner Lyman discloses his profession as a Certified Public Accountant and his interest in the Bluff Dwellings project before joining the other two commissioners in voting to unanimously approve the CRA plan. The next step is to get approval from the taxing entities.

July 2018 – The county commission directs a request for an interlocal agreement to the school board. Berrett attends a July school board meeting in order answer questions about his project. Berrett says that he has approval from the state to open 18 rooms, but says that is not enough to make his business plan work. “We really need to have the 54 units completely open and to have that turning lane installed,” he tells the board.

“One of the criticisms I’ve heard of my project,” Berrett adds, “is, ‘Hey, you’ve already started, we don’t need to help you.’ Well that’s not true. I started with the hope and the prayer we would have the CRA and not knowing exactly how this was going to come about. And I’m still in that position.”

“The reality of the business numbers is 18 rooms won’t work. So even though I started–I’m just impatient. I won’t wait four years for the banks to screw around, I’m going to go out and beat the doors down and I’m going to find a way to do it. That’s just my mentality. That’s how I get stuff done.”

August 2018 – The Bluff Town Council is sworn into office. Any future CRA proposals within the town limits will be reviewed by a Bluff Community Reinvestment Agency, likely the same members as the town council, not the county commission.

Fall 2018 – Present – School board discusses CRAs at their monthly board meetings and develops a rubric for helping determine their interest in CRA projects. Final vote on the Blanding and Bluff projects is pending.

But for?

The question remains: Does the Bluff Dwellings project pass the “but for” test? The county commission seemed to think so when the approved the CRA in May. Now the school board must answer that for themselves. Berrett told them that without the CRA, the buildings currently under construction will become a “vacant project.”

“Honestly, if we don’t get a turning lane,” he said, “I’ll close that thing down, I’ll go bankrupt, and I’ll move somewhere and teach.”

If CRAs are often designated to revive blighted areas in cities or towns, there is an irony to the Bluff Dwellings situation. The land was not blighted before development began, but now, if the CRA isn’t approved, the owner says it will cause the resort to be abandoned. A few acres of half-finished buildings decaying at Bluff’s iconic Cow Canyon entrance could indeed become a blight.

Even though the CRA decision is still pending before the school board, the Bluff Dwellings website promises a grand opening of 54 rooms in fall of 2019. So there does still seem to be a chance for a favorable outcome for both Berrett and San Juan County schools, even without the CRA’s approval. Is it possible that he would be able to secure funding elsewhere, open his resort, and hire 20 new people anyway? In that case, the $450,000 in tax revenue that the business creates will flow directly to the school district over the next 15 years, providing much-needed teacher salaries and school funding. Or will the project indeed fall into bankruptcy “but for” the CRA’s approval? That’s the $450,000 question.

Whatever the outcome, there is a lesson here. If the Bluff Town Council one day decides to create a Community Reinvestment Agency, it could become an important tool for incentivizing certain projects the council wants to support. But future developers should be discouraged from breaking ground on a project that hinges on an unapproved CRA. Students and property owners in the San Juan School District do not benefit from a situation where a developer, intentionally or not, uses the threat of an abandoned construction project as leverage to receive tax benefits. A potential guideline for future Bluff CRAs: Tax incentives will be considered but for when they begin to resemble bailouts.